Would you like to save this?

‘Everything has gone up’: Retirees feel burdened by inflation as home insurance cost surge

Despite their reputation as a financially privileged generation, millions of baby boomers are slipping through significant cracks in the U.S. retirement system. A new source of financial strain on retiree budgets is homeowners insurance premiums, which have skyrocketed by 20% between 2021 and 2023.

Between 2024 and 2030, 30.4 million Americans will turn 65. More than two-thirds of this final baby boomer cohort will be “financially challenged” in retirement, according to the Alliance for Lifetime Income.

The U.S. inflation rate, which surged to 9% in June 2022, has slowed to 2.44% as of September 2024—but years of price increases have wreaked havoc on retirees’ budgets, requiring them to scale down significantly in their golden years. The early-August stock market plunge, which affected 401(k)s, stoked more financial anxiety.

Rising home insurance compounds other soaring costs, like surging car insurance premiums (which increased by 15% in the first half of 2024), grocery price hikes (up 11.4% in 2022 and 5% in 2023), and hospital care costs (up by 7% year over year, as of July 2024).

These increases are especially difficult for the one-third of senior citizens who reported not having enough money to live comfortably in retirement in a 2023 Gallup survey. Insurify‘s data science team analyzed the rising costs of essentials, including home insurance in every state, to find out how inflation is affecting retirees in 2024.

Key Takeaways

- The average annual retirement income is $31,390, according to the most recent. Census Bureau American Community Survey.

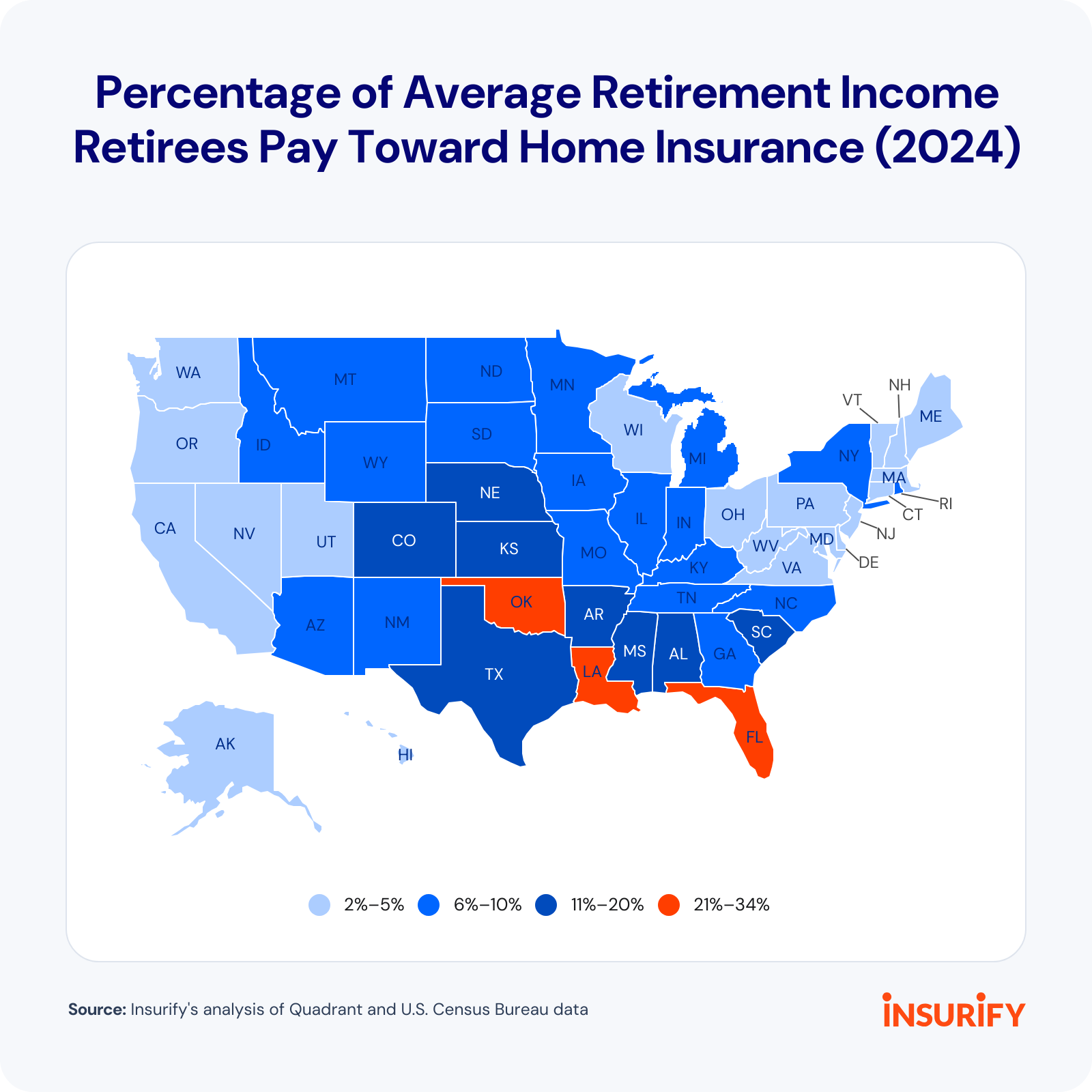

- Florida retirees spend 34% of their average income on home insurance, according to Insurify’s analysis of Quadrant and Census Bureau data. Nationally, retirees pay 8% of their income toward home insurance.

- “Inflation lessening the value of assets” is a top concern for 89% of retirees in Schroders’ 2024 U.S. Retirement Survey, with 68% of retirees concerned about outliving their assets.

Retirees Spend More Than 10% of Retirement Income on Home Insurance in 11 States

The average annual retirement income, including Social Security, pensions, assets, and earnings, is $31,390, according to the latest Census Bureau American Community Survey. American retirees spend 8% of their income on the average home insurance premium.

Coastal states are popular retirement destinations, but they often have serious climate risks that drive up home insurance premiums. Hurricane-prone Florida’s $11,163 average annual home insurance cost equals 34% of the average retirement income for the state. Louisiana retirees face the second-highest home insurance costs in the U.S., at $6,560 annually, representing 24% of their average retirement income.

Moving inland won’t necessarily help retirees stretch a fixed income. While Idaho and Michigan retirees previously paid 7%–8% of their retirement income toward home insurance—aligning with the national average—premiums have increased by 18% and 12%, respectively, in just the first half of 2024.

Both states experience frequent thunderstorms and hailstorms, which lead to costly claims for insurers and drive up home insurance premiums. High insurer loss ratios and building material costs also compound the climate risks in these states, leading to overall higher home insurance rates.

Retirees Are Still Flocking to Florida Amid Ongoing Insurance Crisis

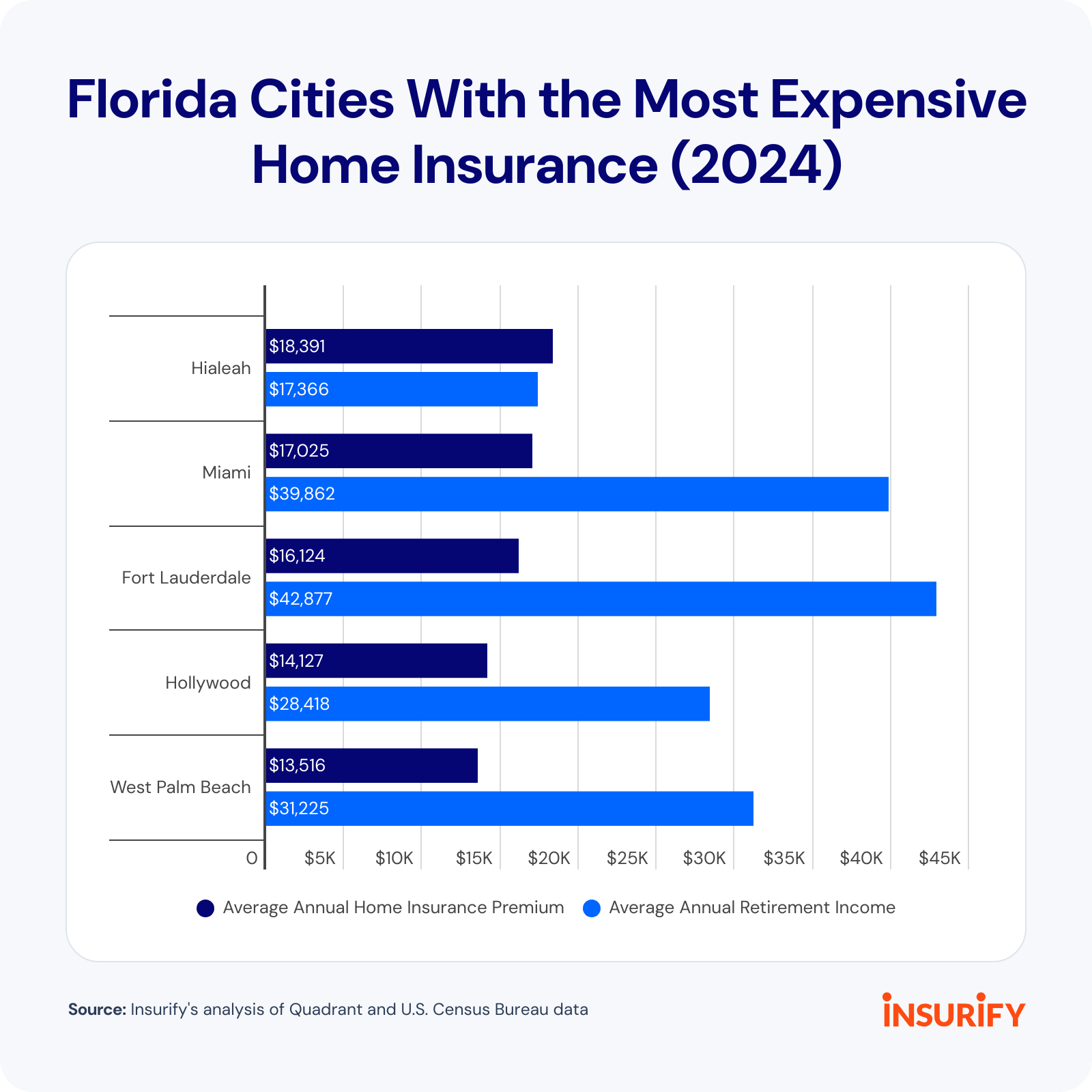

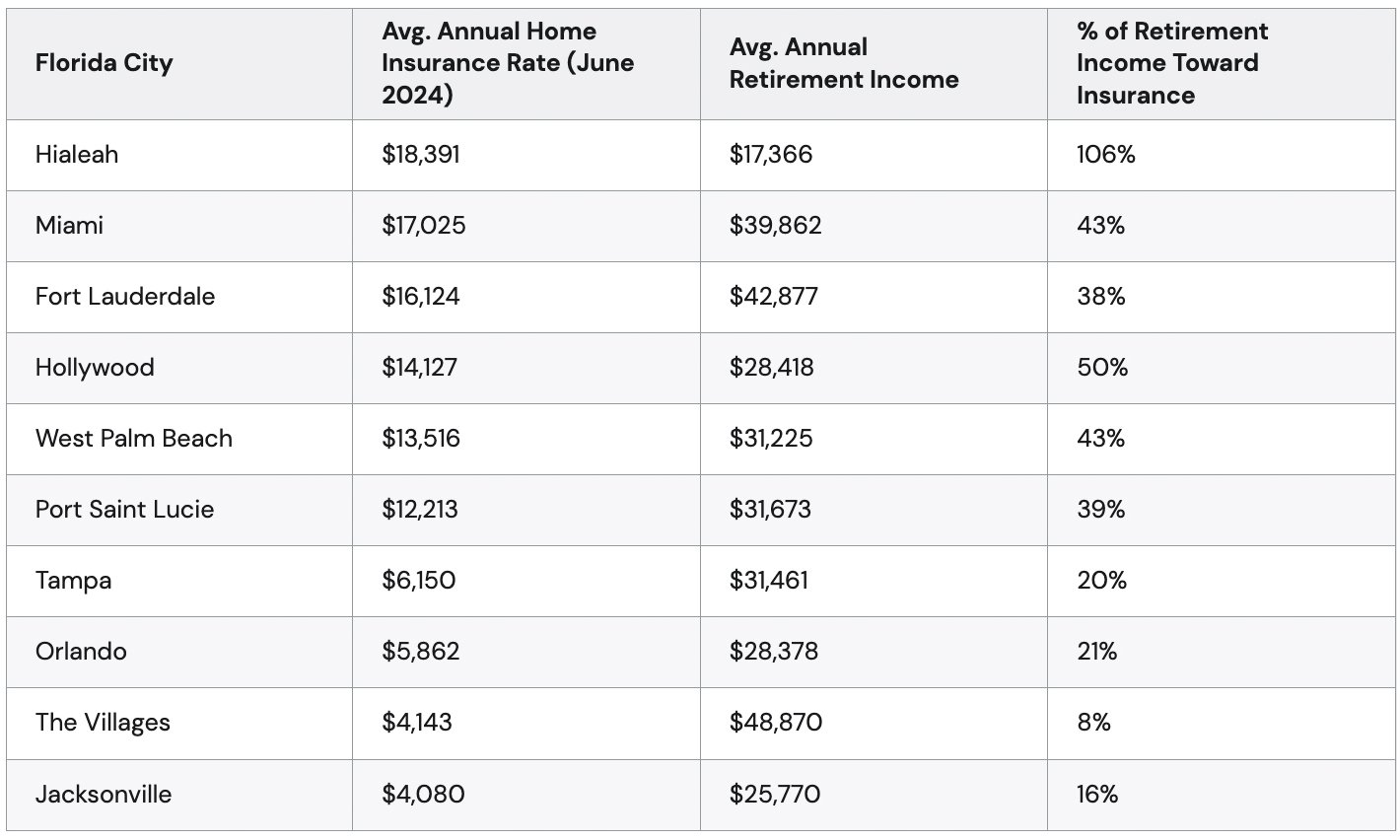

Florida attracted 11% of retirees who moved across state lines to retire in 2023, according to a study by the moving services marketplace HireAHelper. Many of those retirees will find themselves burdened by home insurance costs. Average yearly premiums in one Florida city (Hialeah) exceed the average annual retirement income.

Despite Rising Insurance Costs, Florida Remains a Popular Retirement Choice

Still, the Sunshine State’s sky-high insurance rates aren’t driving away retirees, says South Florida REALTOR® Désirée Ávila. “The insurance rates are crazy, but I don’t see it as a major impediment at this point. The retirement communities keep popping up everywhere and they sell very quickly.”

About one-third (32.8%) of Florida residents age 65 and older live in rented housing, but 67.2% own their homes—slightly exceeding the 65.2% nationwide ownership rate—according to Census Bureau data.

Insurance Crisis Drives More Floridians to State Coverage

As premiums surge and some insurers leave the state entirely, Florida’s ongoing insurance crisis has pushed 1.2 million residents to Citizens Property Insurance Corp., the state’s insurer of last resort. Citizens’ board of governors recently approved a 14% rate hike, effective Jan. 1, 2025, if the Florida Office of Insurance regulation approves the hike.

Ávila doesn’t think the double-digit rate hike will hamper the Florida real estate market, despite a few buyers backing out due to high insurance costs. Instead, she says the policies favor cash buyers, who make up about half of her deals now.

These cash buyers, who aren’t required to carry insurance by a mortgage company, sometimes accept the risk of astronomical hurricane damage and choose to forgo costly home insurance, says Ávila.

Rather than buying a home at the top of their affordable range, Ávila advises Florida transplants to “be very conservative in your budget … so you have that extra cushion” for rising insurance costs.

“We’re definitely in an insurance crisis, and I don’t want to play that down, but I don’t see it hindering people moving to Florida. Florida is still desirable to a lot of people,” says Ávila.

‘It’s Hard to Get By’ for the 21% of Retirees Living Solely on Social Security

As Americans become increasingly concerned about Social Security’s solvency, they might be underestimating how much they’ll rely on it someday.

Nearly 60% of current retirees listed Social Security as a major source of income, but just 34% of non-retirees think they’ll depend on it, a 2023 Gallup poll found. Nearly half (48%) of non-retirees think a 401(k) or IRA will be a major source of income, but only 27% of current retirees say the same.

Carla Jenkins, a 79-year-old from South Central Ohio, is among the 21% of retirees who, according to the Federal Reserve, rely on Social Security as their sole source of income.

Jenkins taught part-time aerobics classes at the YWCA for 35 years but stopped after a shoulder injury. She took another job as a school cafeteria substitute, and her husband was a self-employed barber. Neither of their jobs provided a pension or 401(k).

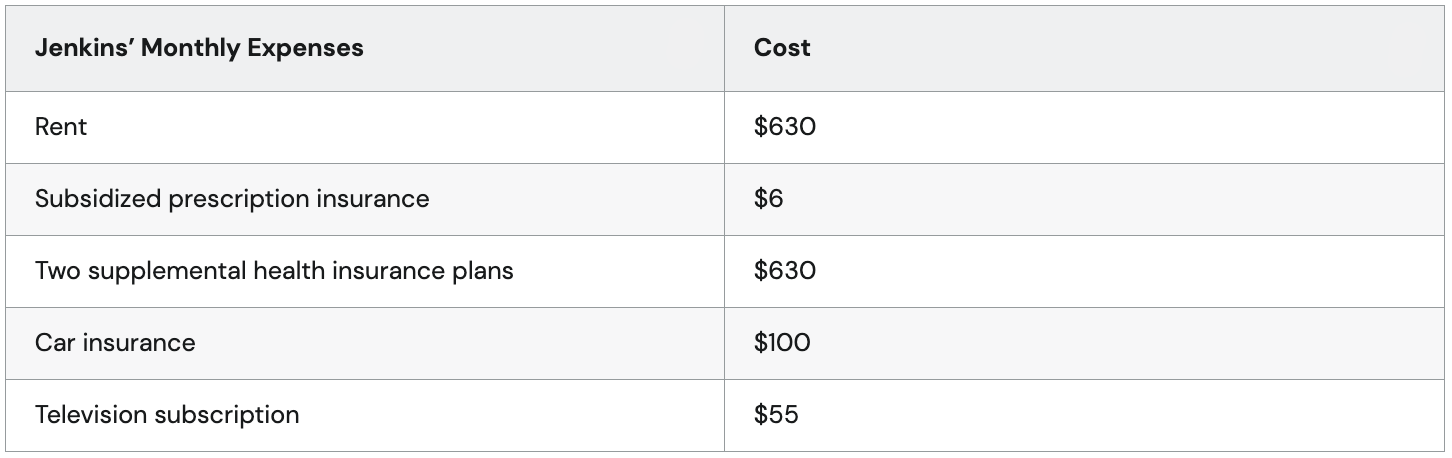

Now, the couple lives month-to-month on a single payment of $1,918, which Jenkins budgets down to the penny. Her expenses include rent for a low-income senior apartment and expensive supplemental health insurance plans. Jenkins hesitates to cancel the policies because they cover costly medical visits, but the premiums make her feel “insurance poor.”

The cost of medical care services increased by 3.3% over the past year, and hospital services, specifically, are up by nearly 7%, per the July 2024 Bureau of Labor Statistics Consumer Price Index, or CPI.

Jenkins also pays $100 monthly for car insurance. Rising costs forced the couple to give up their second vehicle. Auto insurance is typically cheaper for seniors, but Ohio premiums increased by 22% in the first six months of 2024, according to Insurify data. Full-coverage costs increased by 15% nationally, pushing the U.S. average annual premium to $2,329.

The couple spends $1,366 per month (or 71% of their Social Security income) on essentials before buying groceries—an expense that’s risen by 25% over the past five years, according to the CPI. They allow themselves a minor luxury—the lowest-tier AT&T television subscription—but any unexpected expense puts small comforts on the chopping block.

Rising Costs Force Retirees to Make Tough Spending Choices

Jenkins, who doesn’t have dental insurance, recently used CareCredit to pay for a partial bridge. She paid her remaining balance of $201.99 when she noticed incidental charges, like for paper billing, were adding up—but the payment cut into her limited budget, so she had to defer a chiropractor appointment. She also put off buying a $12 skin-calming cream.

These daily calculations are an exhausting reality for the 10.9% of retirees who, according to Census Bureau data, live in poverty.

The SSA increased payments by 8.7% in 2022—the largest cost-of-living adjustment in 42 years.

Jenkins says these increases have made little difference to her financial situation. “When they raise your Social Security, it doesn’t really matter, because that’s also when your rent, and health insurance, and electricity go up.”

The price of necessities has risen 36% faster than other goods and services over the past 60 years, according to the Brookings Institution. The public policy organization’s findings imply that purchasing power for low-income families has eroded significantly faster than standard price indexes, which include non-essential goods and services, suggest.

“It’s hard for us to get by. Everything has gone up,” said Jenkins. “I have to pay attention to everything. I just have to be careful.”

Boomers Facing Housing Insecurity Are Taking in More Roommates

Boomers are the fastest-growing segment of renters looking for a roommate, according to the room-sharing site SpareRoom.

Room sharers and seekers aged 65 and older increased by 525% between 2014 and 2023. In comparison, the number of 35- to 44-year-olds looking for a room or roommate increased by 63%, and the share of 18- to 24-year-olds decreased by 39%.

Nonprofit senior homeshare programs pair older adults with roommates, but the programs often serve a small number of retirees. The New York Foundation for Senior Citizens’ homeshare program, for instance, places about 50 roommate matches annually.

Senior homeowners are more likely to rent out a room in their homes than move in with a roommate, says Matt Hutchinson, director of communications at SpareRoom. “For people who want or need to stay put but are struggling financially, [renting out a room] can be a great option.”

The average monthly price of rent has increased by 29.4% since the beginning of the pandemic, reaching $1,958 at the start of 2024, according to Zillow. About 35% of Americans aged 65 and older live in rentals.[6]

“When you think about how many hours you’d need to work in a second job to generate that level of income, having a roommate makes a lot of sense. Plus, there are social benefits, like company, particularly for older homeowners,” said Hutchinson.

Some Retirees Can Cut Costs, But Others Are Stuck ‘Between a Rock and a Hard Place’

As Americans face skyrocketing auto and home insurance premiums, rising rent, inflated grocery prices, and surging medical care costs, one-third of retirees Gallup polled in 2023 don’t think they have enough money to live comfortably in retirement.

Gloria Garcia Cisneros, a certified financial planner and wealth advisor with LourdMurray, encourages financially strained retirees to use their current assets to increase their income, from renting out a room to liquidating unused cars or collectibles. Low-income retirees may also need to reduce their expenses.

“When you’re making so little, it’s really hard. [One] option would be downsizing their home, or there are reverse mortgages. A reverse mortgage will buy back your house and give you a stream of income for a certain amount of time, but at the end of it, [lenders] keep the house,” said Cisneros.

Retirees can save on home insurance by comparing rates with multiple companies or making weather-resistant upgrades to their homes, which can reduce premiums.

“There are several low-cost upgrades, home repairs, and last-minute prep actions that are both affordable and can be helpful in preventing storm damage,” said Dr. Ian Giammanco, lead research meteorologist for the Insurance Institute for Business & Home Safety.

Giammanco recommends cleaning and securing gutters, downspouts, and soffits, trimming back tree branches, and sealing exterior gaps around windows and doors with silicone caulk to mitigate storm damage. Homeowners can also create a detailed list of belongings to make filing claims easier.

Retirees like Jenkins, who already downsized from a home to a low-income rental and dropped a vehicle to save on insurance, have fewer options.

“A lot of Americans, sadly, are in a situation where it’s like, what do you do? You’re between a rock and a hard place,” said Cisneros.

Methodology

Homeowners insurance rates in this report represent the average annual HO-3 insurance premium for retired 67-year-old homeowners with good credit and zero claims within the past five years. Rates reflect policies for a single-family, frame house with the following coverage limits: $300,000 dwelling, $300,000 liability, $25,000 personal property, $30,000 loss of use, and a $1,000 deductible.

Insurify gathered Quadrant rates for the 10 largest cities in every state. Statewide costs reflect the average rate for homeowners across these ZIP codes. The prices reflect rates as of June 2024. Car insurance data comes from Insurify’s database of more than 97 million quotes and reflects a clean driving record and average or better credit. Median retirement income data are from the Census Bureau’s 2022 American Community Survey.

This story was produced by Insurify and reviewed and distributed by Stacker.

By Cassie Sheets